Survey 2018-19 aims 8% growth for coming 5 years

The Economic Survey 2018-19, led by Nirmala Sitharaman, Minister of Finance, and Krishnamurthy V. Subramanian, Chief Economic Adviser, Government of India, has laid out a plan to achieve a US$5 trillion economy by 2024-25, compared with the current US$2.6 trillion.

The Economic Survey for the fiscal year 2018-19, tabled by India’s Finance Minister Nirmala Sitharaman in the Parliament on July 4th, presented a progressive plan to achieve a US$5 trillion economy by 2024-25, compared with the current US$2.7 trillion. This valuation, the survey said, can be achieved with an 8 per cent annual growth in the national gross domestic product (GDP) over the coming five years. One of the fastest-growing major economies in the world, India is estimated to have grown by 6.8 per cent during fiscal 2018-19. Meanwhile, the GDP growth during the last five years topped 7.5 per cent defining a new normal for the Indian economy. With a stable political environment and improving investment across the economy, India is expected to achieve renewed momentum following a slowdown in the aftermath of certain national policy enactments and global market weaknesses. In the current financial year 2019-20, the Indian economy is expected to record GDP growth of 7 per cent.

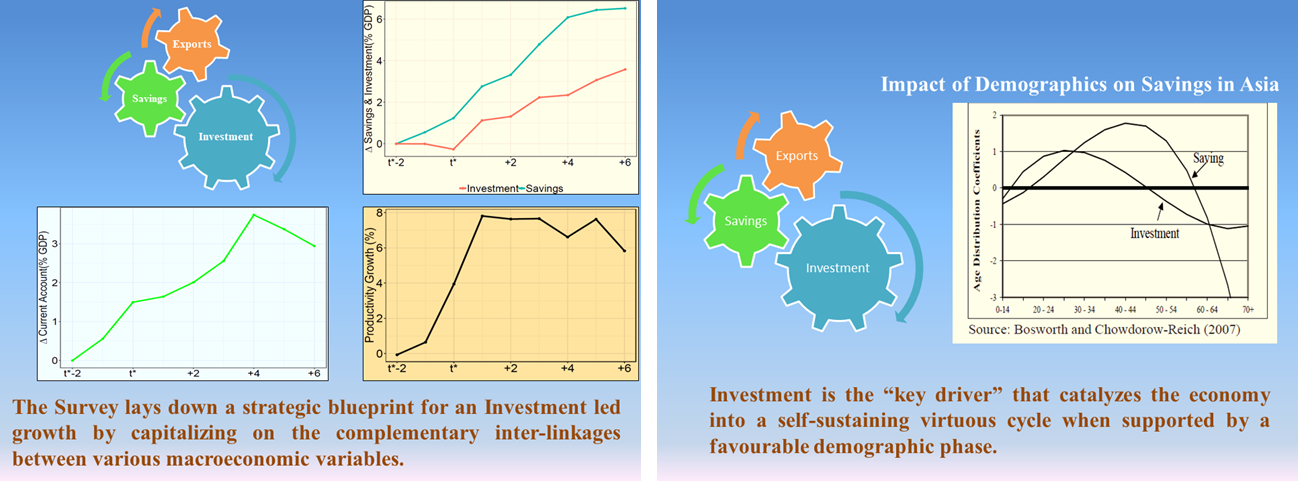

Learning from the global financial crisis, India’s Survey 2018-19 departed from the traditional thinking by viewing the economy as being either in a virtuous or a vicious cycle, and thus never in an equilibrium. Rather than viewing the national priorities of fostering economic growth, demand, exports as well as job creation as separate issues, the Survey approached the macroeconomic phenomena as complementary to each other. The Survey suggested that by driving the virtuous cycle with investment, especially private investment, as the main driver can enable growth in each of the important macro variables - inclusive economic growth, export activity, consumer demand, capacity building, and technology integration. The Survey also sought to strengthen the economy by encouraging entrepreneurship and setting up of micro, small and medium enterprises (MSMEs). Besides creating new jobs, this can empower manufacturing and R&D capabilities while ascertaining the best utilisation of resources.

Key achievements of Indian Economy

- The Economic Survey states that while world output grew at 3.6 per cent between 2014 and 2018, India took giant strides forward to become the sixth largest economy by sustaining growth rates higher than China. India is expected to become the fifth largest global economy in 2019.

- The average inflation in the five years was less than the inflation level of the preceding five years matching the lowest levels attained in the country’s post-independence history. Current account deficit (CAD) stayed in manageable levels and foreign exchange reserves rose to all-time highs.

- The Economic Survey stated that such scenario emerged from a new institutional framework of constituting of the ‘Monetary Policy Committee (MPC)’ in February 2015 with the mandate to target a headline inflation of 4 per cent with a band of two percentage points on either side.

- The Economic Survey said that discipline was also imposed on the gross fiscal deficit (GFD). The FRBM Act of 2003, which decides the glide path for GFD to GDP target ratio of 3 per cent was empowered 2016 and this ratio declined from 4.5 per cent in 2013-14 to 3.4 per cent in 2018-19.

- Welfare programmes such as Pradhan Mantri Jan Dhan Yojana (PMJDY) and Jan Dhan, Aadhar, Mobile (JAM) trinity secured Direct Benefit Transfers (DBT) of more than US$106.2 billion under various schemes. Presently 55 central ministries offer 370 cash-based schemes under DBT.

- The Survey stated that creation of infrastructure accelerated significantly during 2014-19. While India achieved 100 per cent rural electrification in April 2018, rapid road construction led to over 20 per cent of the existing highway length of 132,000 km being built in the last four years alone.

- Fiscal federalism strengthened significantly when the 14th Finance Commission raised the share of states in the divisible pool of central taxes from 32 per cent to 42 per cent. The launch of GST in July 2017 provided key strengths in implementing cooperative federalism in several areas.

- The Insolvency and Bankruptcy Code (IBC), operationalised in 2017, led to a significant number of non-performing assets being brought under its ambit. Large sums were recovered by creditors from resolution or liquidation, bringing in overall improvement in India’s business culture.

- India reported an 8 per cent year-on-year rise in total exports covering merchandise to services units during 2018-19 to reach US$535.5 billion. Cumulative merchandise exports for the period was valued at more than US$331 billion, registering a positive growth of over 9 per cent.

- In 2018, the Government had adopted a strategy for doubling exports by 2025. Besides aiding economic growth, rising exports have helped in generating jobs and bolstering foreign exchange reserves. India is encouraging entrepreneurship and strategic investment to drive this growth.

- The Economic Survey stated that the banking sector clean-up and IBC framework are important foundations that will now reap benefits when the investment-driven growth model is put into motion. The model implies a rapid expansion in the financial system– banks and capital markets.

- The Survey pointed out that India was ranked 3rd in the world in terms of a start-up ecosystem, adding that systematically lowering the risks faced by investors in India is critical for the success of the investment-driven model for economic growth, along with demand, exports and jobs.

The year 2018 reaped the benefits of Government’s leading economic policies and projects implemented over the last four years that focussed on developing skills as well as providing a range of services to the citizens, including electricity, digital connectivity, healthcare, higher education, banking services, housing and roadways, among others. The last four years also saw a steady rise in indigenous entrepreneurship. After India’s jumping 65 spots to reach the 77th place in the World Bank’s Ease of Doing Business ranking since 2015, the Central Government has launched a similar ranking of its 29 states and seven union territories, with Andhra Pradesh, Telangana, Haryana, Jharkhand and Gujarat grabbing the top five spots. Proactive policy amendments, regulatory measures as well as improved liberalisation, together with the nation’s high-margin and high-quality innovation and production environment, have led to a steady spike in interest of foreign investors when it comes to setting up operations in India.

Note: US$1= 68.66*